Advance Tax & Why It Matters

Neha Navaneeth

Marketing & Content Associate

Taxation

What is advance tax?

Advance tax is the amount of income tax that is paid much in advance rather than a lump-sum payment at the year-end. Also known as earn tax, advance tax is to be paid in installments as per the due dates decided by the income tax department.

The schedule for paying installments of advance taxes is:

Date | Advance tax |

On or before June 15th | Minimum 15% of the total estimated tax liability for the financial year |

On or before September 15th | Minimum 45% of the total estimated tax liability after deducting the tax already paid |

On or before December 15th | Minimum 75% of the total estimated tax liability after deducting the tax already paid |

On or before March 15th | 100% of the total estimated tax liability after deducting the tax already paid |

Who is required to pay advance tax?

Advance tax payment is mandatory for individual and non-individual taxpayers in India if their estimated tax liability for a financial year is equal to or exceeds Rs 10,000. In this regard, taxable liability is calculated after deduction of TDS (Tax Deducted at Source). This is applicable to Non-resident (NRIs) taxpayers as well.

The conditions for advance tax liability for NRIs:

The primary condition is an estimated tax liability of Rs 10,000 or more for a financial year.

Secondly, advance tax is applicable only on income that NRIs have earned, accrued, or received in India. The income earned outside India is not considered for estimating advance tax liabilities in India.

Non-resident Indians trying to estimate their advance tax liability for a financial year must take the following types of income into consideration.

Rental income from a property owned in India

Capital gains from the sale of assets in India

Interest income from NRO accounts in India

Professional income and revenue from business owned and performed in India

Calculation of advance tax liability

Assume Anita is an employee of an Indian IT company. She has been posted in the UK on offshore projects as a software developer for the last 5 years.

She estimates to receive the following income in India during FY 2025-26:

Income from rent property located and owned in India - Rs 8,00,000

Interest earning from fixed deposits in her NRO account - Rs 1,00,000

Long-term capital gains (LTCG) from the liquidation of mutual funds - Rs 5,00,000

The taxable amount of rental income after applying the standard deduction of 30% is Rs 5,60,000.

For NRIs, LTCG over and above Rs 1.25 lakh is taxable at a rate of 12.5%. So, taxable LTCG is (Rs 5,00,000 - Rs 1,00,000) or Rs 4 lakh. The tax liability on LTCG is (Rs 4 lakh * 10%) or Rs 40,000.

The entire interest income from the NRO account is taxable.

So, total taxable income after clubbing rent and interest income is (Rs 1 lakh + Rs 5.6 lakh) or Rs 6.6 lakh.

Considering the default tax regime (new tax regime), Anita’s estimate tax liability will be {(Rs 6.6 lakh * 5%) + Rs 40,000} or Rs 73,000.

As per the scheduled dates of advance tax payments, Anita’s instalments of advance tax payments will be,

Date | Advance tax instalments | Advance tax instalments @ total estimates tax liability of Rs 73,000 |

On or before June 15th | Minimum 15% of the total estimated tax liability for the financial year | Minimum Rs 10,950 |

On or before September 15th | Minimum 45% of the total estimated tax liability after deducting the tax already paid | Minimum Rs 21,900 |

On or before December 15th | Minimum 75% of the total estimated tax liability after deducting the tax already paid | Minimum Rs 21,900 |

On or before March 15th | 100% of the total estimated tax liability after deducting the tax already paid | Minimum Rs 18,250 |

How to pay advance tax?

NRI taxpayers can calculate advance tax liabilities themselves. However, taking help of professional tax consultants (e.g., CA) is advisable if income in India is significantly high and from multiple sources. Besides, tax consultants help maintain tax documents properly. These documents are essential for NRIs taking benefit of tax treaties in their country of residence.

Paying advance tax is easy and is a complete online procedure. A taxpayer does not require to register or login.

Steps to paying advance tax on the income tax portal:

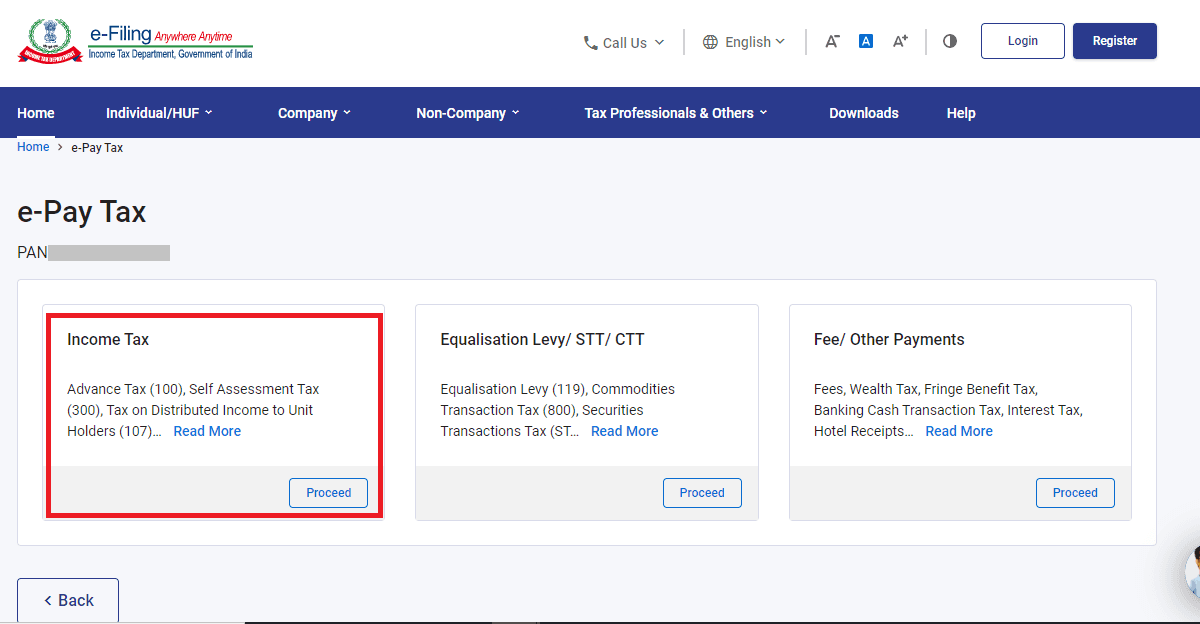

Navigate to e-Pay tax inside https://www.incometax.gov.in/iec/foportal/.

Enter your PAN and mobile number as prompted.

Validate your mobile number using the one-time password (OTP) sent to you.

After OTP validation, you’ll see three sections:

Income Tax

Equilisation Levy

Fee/Other Payments

Select the “Income Tax” section for advance tax payment.

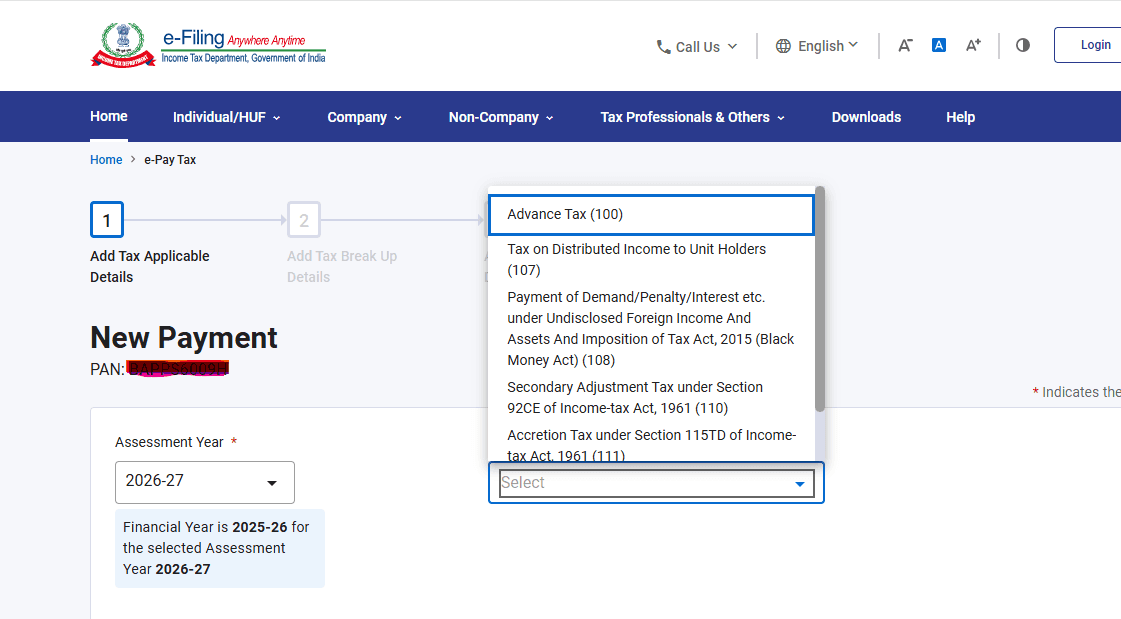

Choose the relevant assessment year.

Select “Advance Tax (code 100)” from the drop-down menu.

Proceed to complete the advance tax payment as instructed.

Consequences of non-payment or late payment of advance tax

The principal penalty for non-payment or late payment of advance tax by NRIs are interest charges at 1% per month on the unpaid amount for the period of the delay or non-payment. A 1% penal rate of interest per month may sound trivial. But it can quickly turn an unpaid tax liability into a hefty cumulative burden through compounding, especially when tax liability is high.

Imagine a tax liability of Rs 10 lakh in India for the financial 2024-25 for Ajay an NRI living in the USA. He filed tax return on 31st July 2025. By this time, he faced a penalty of 4% for missing to pay advance taxes in all the 4 quarters during FY2024-25. Besides, 90% of tax liability remained unpaid during the financial year. This would attract another 1% penal interest charge on the entire liability for the year (under Section 234B).

Total tax liability Rs 10 lakh

Total interest charge under 234B is Rs 40,000/-

Total interest charge under 234C is Rs 25,000/-

So, for Ajay, the total penalty will be around Rs 65,000/-.

Why does it matter for NRIs?

The obvious reasons are avoiding penalties and a sudden lump sum tax burden at the year-end. Additionally, NRIs residing in countries with a Double Taxation Avoidance Treaty (DTAA) with India need to submit their tax paid certificate from the Indian tax authority with their current country of residence. It is essential for claiming DTAA benefits.

Advance tax payment is mandatory for individual and non-individual taxpayers in India with an estimated tax liability of RS 10,000 or above in a financial year. It is not a formality, and failure to comply will attract penal interest charges. Non-payment or delays for prolonged periods of time can accumulate the interest charges to a significant burden through compounding.

Consult with your tax consultant to avoid non-compliance regarding advance tax payment on earnings in India.

Frequently Asked Questions

How do I determine whether I’m classified as NRI or Resident for tax, and why does it matter for advance tax?

Many NRIs confuse their tax status- it's not just about living abroad or having an NRE account. Your tax residency depends on the number of days spent in India during the financial year, and this affects whether your global income or only Indian income is considered for advance tax. Misdeclaring status can lead to major penalties and incorrect advance tax payments.

What documentation do I need to give my CA/tax advisor to avoid mistakes in advance tax computation and DTAA claims?

NRIs often miss or misfile important documents such as passport travel logs, overseas tax certificates, Form 67 (for claiming foreign tax credit), and AIS/Form 26AS reconciliation reports. Properly organized records prevent wrong advance tax payment and maximize treaty benefits.What happens if I select the wrong tax regime (old vs new) or forget to submit the required forms-can my advance tax calculation go wrong?

It’s a frequent error for NRIs to default to the new tax regime when the old regime with its deductions would save significantly more tax. Failing to file Form 10-IEA for regime selection or Form 67 for DTAA can result in excess advance tax, loss of credits, or rejection/penalty after filing.