Am I RNOR? How to Calculate Your Residential Status After Returning to India

Apoorva K

Team Rupeeflo

Taxation

If you've recently returned to India (or are planning to) you've probably come across the term RNOR.

It is one of the most valuable tax benefits available after moving back. RNOR is basically a tax-free window that most NRIs returning to India get a 2–3 year window where their foreign income stays out of the Indian tax net. This includes overseas salary, rent from property abroad, interest in foreign bank accounts, and gains in a US brokerage.

RNOR is considered to be a transitional status under the Income-tax Act that sits between being an NRI and becoming a fully taxable Indian resident.

The challenge? Most people don't know whether they qualify.

Unlike a visa or a bank account, RNOR isn't something you apply for. Your status is determined automatically based on your travel history and India's tax residency rules. That also means many returning NRIs either assume they qualify when they don't, or miss out on the benefits because they never calculate their status correctly.

This guide walks you through the process, step by step.

By the end, you'll know:

Whether you've become an Indian tax resident

Whether you qualify for RNOR status

How to calculate your status using your travel history

How long RNOR can last

What your RNOR status means for your taxes

Let's start with the obvious question.

What is RNOR?

RNOR stands for Resident but Not Ordinarily Resident.

It's a temporary tax residency status that many NRIs qualify for after returning to India.

Think of your journey like this:

Non-Resident (NR) → Resident but Not Ordinarily Resident (RNOR) → Resident and Ordinarily Resident (ROR)

RNOR acts as a transition period between being an NRI and becoming a regular Indian tax resident.

Why does this matter?

Because your residential status determines how India taxes your income.

For example, while you're an RNOR, much of your foreign passive income may not be taxable in India. This includes overseas bank interest, foreign dividends, rental income from property abroad, and gains from overseas investments. Of course, the exact treatment depends on your specific situation and the applicable provisions of the Income-tax Act.

Once you become a Resident and Ordinarily Resident (ROR), India generally taxes your global income, making your foreign assets and investments part of your Indian tax obligations.

A 60-second refresher: NRI → RNOR → ROR

Status | Indian income | Foreign income | What it means in practice |

NRI (Non-Resident) | Taxable | Not taxable | Only income earned or received in India is taxed. |

RNOR (Resident but Not Ordinarily Resident) | Taxable | Mostly not taxable | Your transition buffer: foreign passive income stays tax-free, unless it comes from a business or profession controlled from India. |

ROR (Resident and Ordinarily Resident) | Taxable | Taxable | Full global taxation, plus mandatory foreign-asset disclosure (Schedule FA). |

Your status is determined fresh for every financial year (April 1 – March 31), purely from your day counts. Nobody assigns it to you and there’s nothing to apply for — which is exactly why you can calculate it yourself.

This is why calculating your RNOR status is so important. It tells you whether you're currently in this transitional phase and helps you understand how your foreign income may be treated.

So, how do you know if you're RNOR?

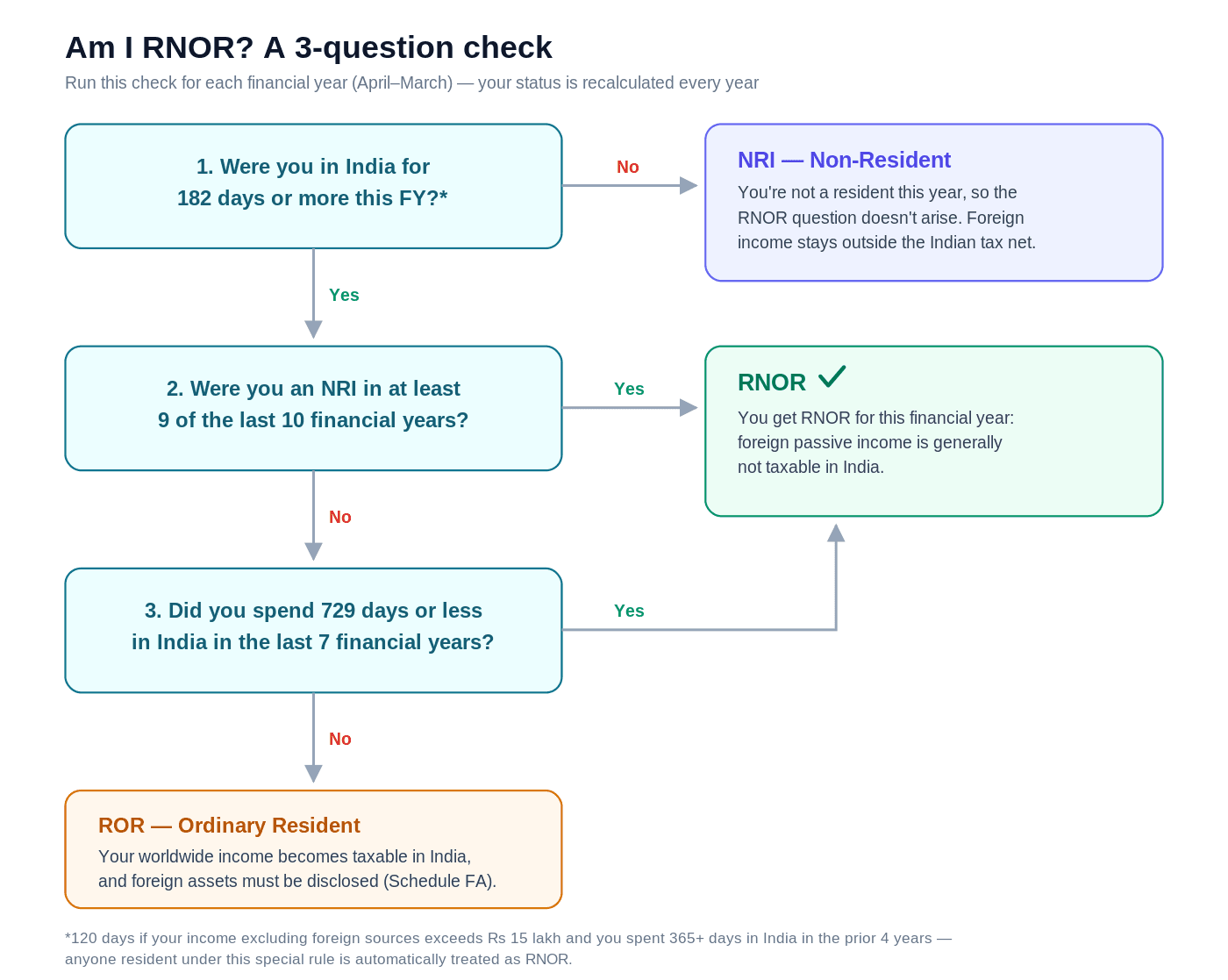

Here’s How to Check if You're RNOR

You can determine your RNOR status by answering two questions.

Question 1: Are you an Indian tax resident this financial year?

RNOR is a sub-category of resident. So before the RNOR question even arises, check whether you qualify as an Indian tax resident for the year under Section 6(1) of the Income-tax Act.

You are a resident if you were physically present in India for:

182 days or more during the financial year, or

60 days or more during the financial year and 365 days or more across the four preceding financial years.

The carve-out for NRIs and PIOs visiting India: the 60-day threshold generally doesn’t apply to Indian citizens and Persons of Indian Origin coming on a visit. Instead:

If your total income (excluding income from foreign sources) is up to ₹15 lakh, the threshold is relaxed to 182 days.

If it exceeds ₹15 lakh, the threshold is 120 days (provided you also spent 365+ days in India across the preceding 4 years). Becoming resident under this 120-day rule automatically makes you RNOR — not ROR.

If you don’t cross either test, you remain a Non-Resident for that year - which is often good news, as you’ll see in the section on timing below. If you are a resident, move to Step 2.

Question 2: Do you pass either RNOR condition?

ou qualify as RNOR if you meet either one of the following two conditions (not both). This is the single most misunderstood part of the rules.

Condition 1: The 9-out-of-10 test

You were a Non-Resident in at least 9 of the 10 financial years immediately preceding the current one. This is how most long-term NRIs qualify.

Example: Rohan moved to California in 2015 and returned in 2026. He was a Non-Resident in all ten preceding financial years, so he qualifies.

Condition 2: The 729-day test

Your total stay in India across the 7 preceding financial years is 729 days or less. This test counts only days - your residency labels for those years don’t matter.

Example: Amit lived in New York for eight years, visiting India about 70 days a year. His 7-year total is roughly 490 days - comfortably under 729. He qualifies.

Counter-example: Sneha left India in FY 2020–21 and returned in FY 2025–26. She fails Condition 1 (only about five Non-Resident years in the last ten) - and she fails Condition 2 as well, because she lived in India full-time for three of the last seven years, putting her far past 729 days. She becomes ROR as soon as she is a resident again.

Either condition is enough. If you fail the 9-out-of-10 test, you may still qualify through the 729-day test — and vice versa. Always check both before concluding you’re not RNOR.

Example: Calculating RNOR Status

Let's walk through a real scenario.

Amrita returned to India permanently in July 2026 after living and working in the US for 12 years. Here's how she would determine her residential status.

Step 1: Is Amrita an Indian tax resident?

From July to March 31, Amrita spends about 274 days in India in FY 2026-27. That's more than 182, so she is an Indian tax resident for the year. On to Step 2.

Step 2: Does Amrita qualify for RNOR?

She checks the two rules. She was a Non-Resident in all 10 preceding financial years, and her occasional visits add up to well under 729 days across the last 7. She only needed one of these; she has both. Amrita is RNOR for FY 2026-27.

What if Amrita had moved abroad in 2023 instead of 2014?

She would still become a tax resident on returning, but she'd fail both RNOR rules: only three Non-Resident years in the last ten, and since she lived in India until 2023, her 7-year day count is around 1,460 days, nearly double the limit. She would become a Resident and Ordinarily Resident (ROR) almost immediately.

How to calculate RNOR yourself

You need one thing: an accurate log of your days in India. After that, it's mechanical.

Pull your travel history. Passport stamps, airline itineraries, or immigration records. Count both arrival and departure days as full days in India.

Build a year-wise table. One row per financial year for the 10 FYs before your return: days in India, and whether that made you Resident (182+) or Non-Resident.

Count your Non-Resident years in the last 10. Nine or more means Condition 1 is met.

Total your days across the last 7 FYs. 729 or less means Condition 2 is met.

Statuses are recalculated every year on a rolling basis, so repeat this for each future year. Or skip the spreadsheet and use our free RNOR calculator [link when live], which does the year-by-year math from your return date and travel history in seconds.

The key takeaway

Don't focus on how many years you've lived abroad. Instead, answer these three questions:

Have you become an Indian tax resident?

Were you a Non-Resident for 9 of the last 10 financial years?

Did you spend 729 days or less in India during the previous 7 financial years?

Your answers will usually tell you whether you're NR, RNOR, or ROR.

How Long Does RNOR Last? (Usually 2 years. 3 at most!)

This is one of the most common questions returning NRIs have, and the answer often surprises them.

There isn't a fixed RNOR period. Unlike a visa that's valid for a set number of years, your RNOR status is determined separately for every financial year. You don't automatically get RNOR for two or three years after returning to India; your eligibility is recalculated every year using the same rules discussed above.

Here's why two years is the ceiling for most people. Each year, the 9-out-of-10 test looks at the 10 years behind it. In your first two years back, your NRI years still fill that window. By year three, your own post-return resident years have crowded them out, and the test fails. The 729-day test rarely rescues you either, because your first full years back in India add 300+ days each to the count.

What this means for different situations:

Your situation | Likely outcome |

|---|---|

You lived abroad for 10+ years and visited India only occasionally | Typically two RNOR years after returning |

You frequently visited India while living abroad | Your RNOR period may be shorter, because you've already accumulated more days in India |

You lived abroad for only a few years before returning permanently | You may not qualify for RNOR at all and could become ROR soon after becoming a tax resident |

Planning tip: Estimate your RNOR window before relocating. It shapes when to sell foreign investments, take retirement distributions, and restructure assets. More on this below.

Why your return date matters more than you think

Whether the year of return itself becomes your first RNOR year depends on when you land:

You return in… | Year of return | Your RNOR years |

|---|---|---|

April–June | Resident (182+ days). RNOR year 1 used up immediately | Return year + 1 more |

July–September | Usually Resident | Return year + 1 more |

October onwards (under 182 days left in the FY) | Stays NRI | The two following FYs |

Returning in the second half of the financial year shifts your whole RNOR window one year later: you stay NRI for the year of return (foreign income untaxed) and then get two full RNOR years. If your move date is flexible, landing after early October is usually the better deal. In Amrita's case above, waiting from July to October would have bought her an extra NRI year before her RNOR clock started.

Can you stretch it to 3 years?

Only through the 729-day test, and only with deliberate planning: short pre-return visits, plus 2 to 3 months outside India each year even after returning, so your rolling 7-year day count stays under 729 into a third year. For most people this isn't practical. Plan around 2 years.

What's taxable during your RNOR years?

The short version: your Indian income is taxable; your foreign income generally is not, unless it comes from a business or profession controlled from India. In detail (per Section 5 of the Income-tax Act):

Nature of income | RNOR treatment | Examples & notes |

|---|---|---|

Received (or deemed received) in India | Taxable | NRO account interest; any income credited directly to an Indian bank account. Remitting money you already received abroad is not "receipt in India". |

Accruing or arising in India | Taxable | Salary for work done in India (even if paid into a foreign account); rent from Indian property; capital gains on Indian stocks, mutual funds, or real estate. |

Foreign income from a business controlled / profession set up in India | Taxable | You run a Dubai consulting firm but take the management decisions from India. That income is taxable. |

All other foreign income | Not taxable | Foreign salary and rent; interest from foreign banks; overseas capital gains and dividends; 401(k), IRA, or UK pension distributions received abroad. |

What should you actually do during your RNOR window?

The RNOR years are a planning window, not just a tax break. Before ROR arrives:

Review overseas investments. Gains realized while RNOR generally escape Indian tax; the same gains realized after becoming ROR won't.

Decide on foreign retirement accounts. Understand how your 401(k)/IRA distributions will be taxed once you're ROR, and whether to withdraw or restructure earlier.

Prepare for Schedule FA. From your first ROR year, every foreign asset (bank accounts, brokerage accounts, stock options, property) must be disclosed in your Indian return. Start the inventory now.

Map your DTAA relief. Where income will be taxed in both countries, know which treaty credits you can claim.

Talk to a cross-border CA before your final RNOR year ends, not after.

When RNOR ends

The transition to ROR changes your tax life materially. India begins taxing your worldwide income, including US dividends, brokerage gains, and retirement distributions, with DTAA credits available for foreign taxes paid. Schedule FA disclosure of all foreign assets becomes mandatory, with severe penalties under the Black Money Act for omissions.

Common mistakes returning NRIs make

Using calendar years instead of financial years. Everything runs April 1 to March 31.

Confusing FEMA residency with tax residency. FEMA governs your bank accounts (NRE/NRO conversion, see our guide [internal link]); the Income-tax Act governs your taxes. The definitions differ: FEMA status can change the day you return, while tax status waits for day counts.

Ignoring arrival and departure days. Both count as full days in India.

Assuming both RNOR conditions must be met. Either one is enough.

Waiting until ROR to plan. The window to restructure foreign assets tax-efficiently is the RNOR period itself.

FAQs

Do I need to apply for RNOR status?

No. It's determined automatically from your travel history each year; there's no form or approval. You simply declare the correct status in your tax return.

How long does RNOR usually last?

Two financial years for most returning NRIs. A third year is possible only via the 729-day test, with careful planning of your India days.

Can I lose RNOR status earlier than expected?

Yes, if you spent more days in India during the lookback years than you assumed. Recount from passport stamps before relying on it.

If my flight lands at 11:30 PM, does that day count toward my stay?

Yes. Arrival and departure days both count as full days of physical presence.

Can my spouse keep RNOR status after I become a full resident?

Yes. Residency is tested individually; each person's own travel history decides.

What happens to my US 401(k) withdrawals after RNOR ends?

Once you're ROR, distributions become taxable in India, with DTAA credit for US tax already paid.

Does RNOR mean I don't need to file an Indian tax return?

No. If your Indian-sourced income exceeds the basic exemption limit, you must file. RNOR changes what's taxed, not whether you file.

Disclaimer: Tax laws and residency definitions are subject to change. This guide is for informational purposes only and does not constitute tax or legal advice. Verify your travel logs and financial structures with a qualified chartered accountant before filing.